Entrepreneurship promotion 3

Why is it useful?

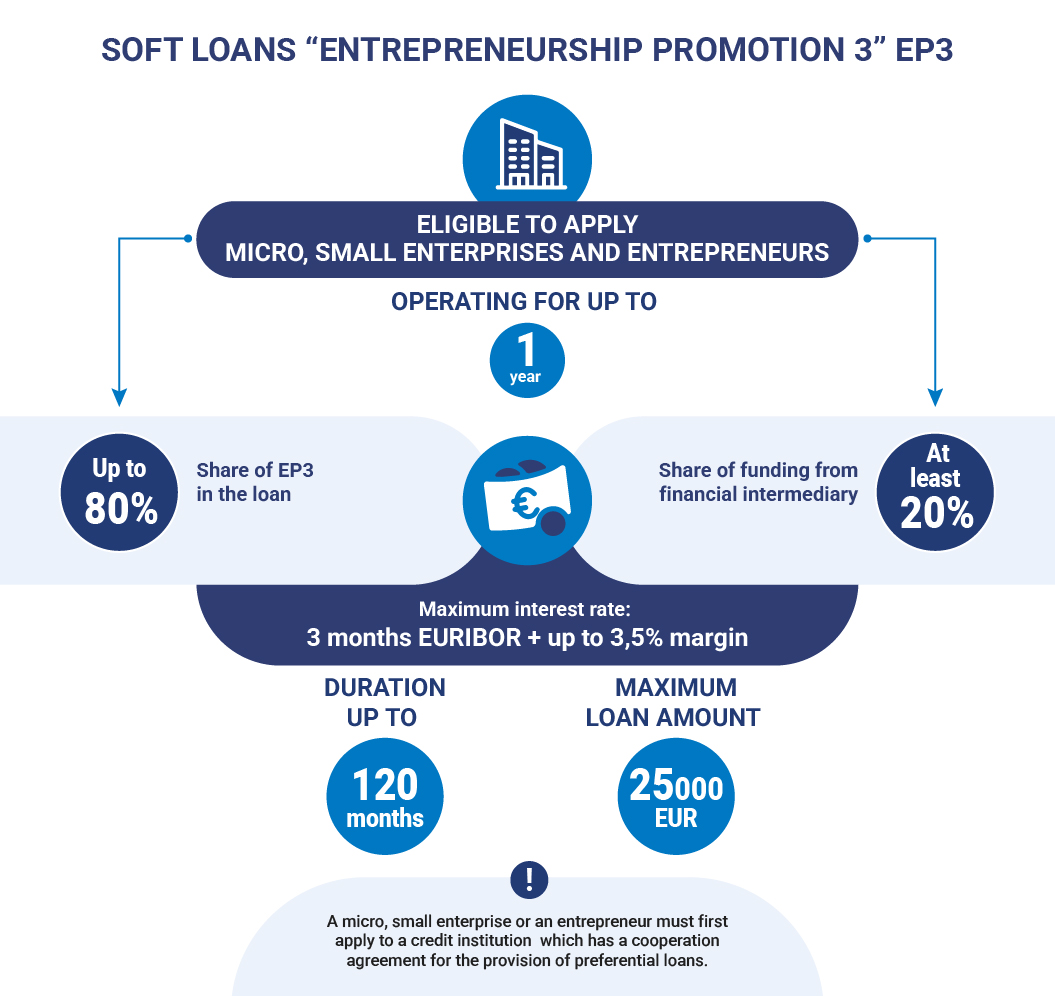

The incentive financial instrument Entrepreneurship promotion 3 (EP3) facilitates access to finance for micro, small and entrepreneurial enterprises to start or develop a business of up to one year. Soft loans are available for investment and/or working capital.

Who can apply?

Micro, small enterprises and entrepreneurs who qualify as an SME under the SME law and have been registered and operating for no longer than one year (calculated from the date of registration of the enterprise in the Register of Legal Entities. In the case of an entrepreneur, this is the date of registration of the business licence or certificate of individual economic activity with the State Tax Inspectorate, to the date of submission of the application for a loan).

The selection of financial intermediaries is currently underway. The list of credit institutions that will be possible to apply will be published once the cooperation agreements have been concluded with them.

The selection of financial intermediaries is currently underway.

How much?

EUR 29 million is allocated for the implementation of the EP3 from the Entrepreneurship Promotion Fund 2014–2020 financed by the European Social Fund.

The maximum loan amount is EUR 25,000. No more than two loans may be granted by a single financial intermediary to a single borrower during the whole period.

The share of the EP3 in any one loan cannot exceed 80% and the share of the financial intermediary’s own funds in any one loan must be at least 20% ( default risk is shared in the same proportion).

Maximum interest rate: 3 months EURIBOR + up to 3.5% margin.

Terms

Loans are for a maximum period of 120 months.

The financial intermediary may sign loan agreements with borrowers until 31 December 2027 (with the possibility of an extension).

How does it work?

To use EP3 loans a micro, small enterprise or an entrepreneur must first apply to a credit institution which has a cooperation agreement for the provision of soft loans.

The provision of loans to borrowers under the EP3 instrument is de minimis aid to which the provisions of Article 5 of Commission Regulation (EU) 2023/2831 apply.

Loans are to finance investments and/or to make up shortfalls in working capital, where such financing relates to the start-up of a new activity or to the maintenance, strengthening or expansion of an existing activity.

Loans are for investment when the portion of the loan to finance the investment is at least 51% of the total amount of the loan, and the remainder of the loan may be used to replenish working capital shortfalls. In all other cases, the entire loan is deemed to be for the purpose of replenishing the working capital shortage.

- In the cases referred to in clauses (1) and (2) of Article 1 of Commission Regulation (EU) 2023/2831:

- The payment of dividends and/or royalties, for capital reduction by way of disbursement to the Borrower’s participants, for the repurchase of the Borrower’s own shares or for other payments out of the Borrower’s capital to the Borrower’s participants. Nor may it be used for the purpose of repayment of loans, or for the granting of loans to, acquisition of or investment in other legal persons or other natural or legal persons, and/or for the acquisition and/or financing of financial assets. Financial assets are defined as cash and cash equivalents, securities of other entities, contractual rights to receive cash or cash equivalents, and derivative financial instruments.

- Refinancing the Borrower’s existing financial liabilities, i.e. to prepay or refinance the Borrower’s existing liabilities to financial institutions (including INVEGA), as well as to reimburse liabilities owed to other parties under loan agreements.

- For the purchase and/or construction and/or installation of residential immovable property and/or for investments in the substantial improvement of a residential building/structure, as defined in the Value Added Tax Law of the Republic of Lithuania.

- For land purchases where more than 10 per cent of the loan proceeds are committed.

- For the purchase of non-commercial vehicles, except for borrowers whose main and activity actually carried out is car rental, as well as services provided by driving schools, passenger transport, including taxis and transportation. This applies to cases of purchase of special-purpose vehicles, as specified in point 18 of the requirements for motor vehicles and their trailers according to their categories and classes according to construction. Approval is by the Director of the Transport Safety Administration of Lithuania, approved by the 2 December 2008 Order No. 2B-479 ‘On the approval of the Requirements for motor vehicles and their trailers according to their categories and classes according to construction’. The activity of renting cars is deemed to be effectively carried out when such services are publicly offered on the market.

- Purchase of cargo vehicles, as defined in the Road Transport Code of the Republic of Lithuania, for borrowers engaged in the activity of road carriage. This is providing freight transport services for remuneration (activity code according to the Classifier of types of economic activity Rev. 2 is class 49.41) and/or renting such vehicles (activity code according to the Classifier of types of economic activity Rev. 2 is subclass 77.12.10).